Despite recent gains, significant events lie ahead. The Fed’s policy path is uncertain, the presidential election remains tight, and worsening geopolitical conflicts could impact global stability, supply chains, and oil prices. Market volatility is always a possibility, especially with elevated valuations and earnings expectations. Below, we outline five key factors driving the market and their potential implications for investors in the coming months.

Despite recent gains, significant events lie ahead. The Fed’s policy path is uncertain, the presidential election remains tight, and worsening geopolitical conflicts could impact global stability, supply chains, and oil prices. Market volatility is always a possibility, especially with elevated valuations and earnings expectations. Below, we outline five key factors driving the market and their potential implications for investors in the coming months.

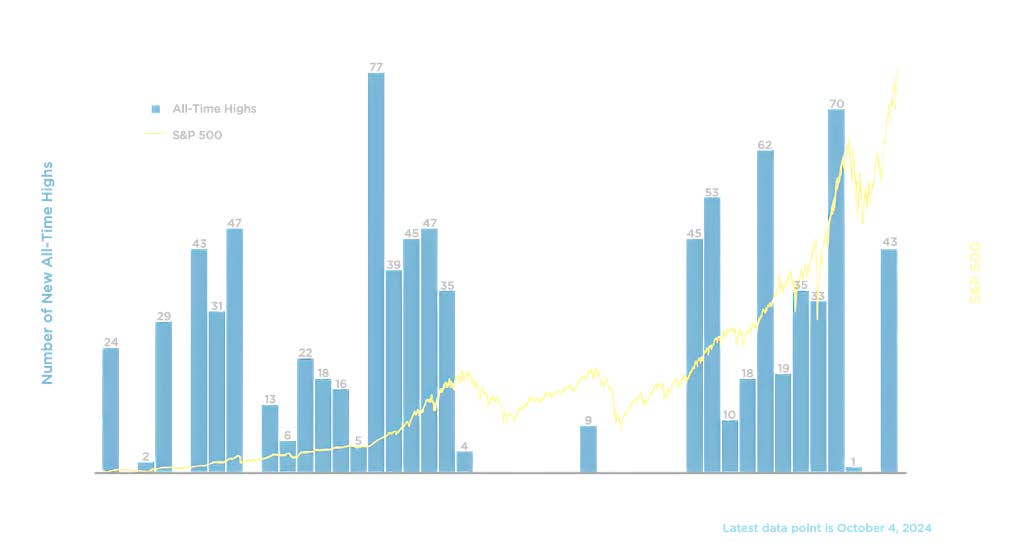

- The market achieves many new all-time highs during bull markets

The market has reached multiple new all-time highs this year, including in the past quarter. While encouraging, this can cause concern among investors who fear a potential pullback. However, during bull markets, it’s common for stock indices to hit new highs, driven by sustained earnings, economic growth, and positive investor sentiment.

Historically, new all-time highs have not reliably predicted pullbacks; it’s the underlying market and economic trends that matter most. Attempting to time the market based solely on index levels is often counterproductive for this reason.

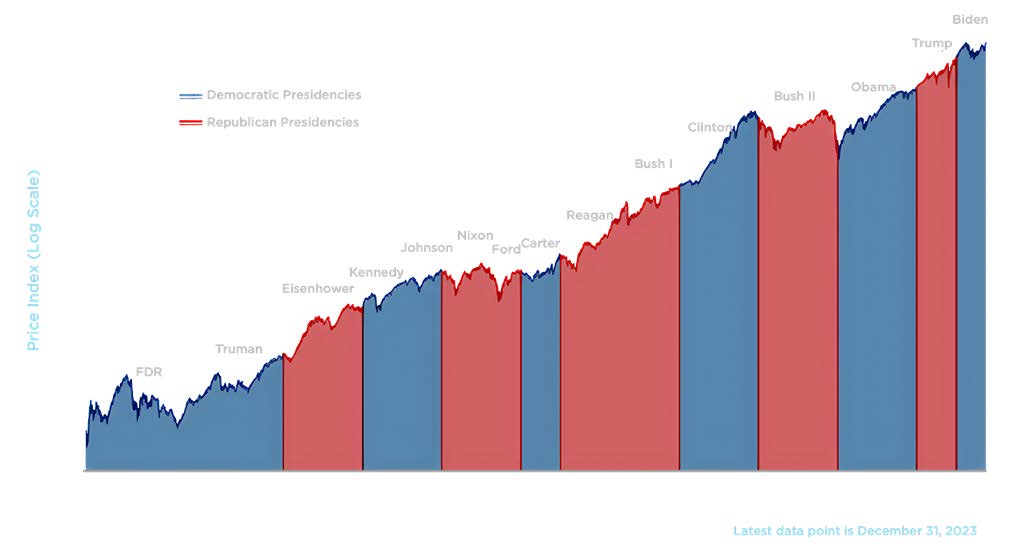

2. The market has performed well under both political parties

2. The market has performed well under both political parties

Second, many investors are concerned about the potential impact of the presidential election on the economy. History shows that the stock market has experienced long-term growth under both major political parties, as seen in the accompanying chart. It is not the case that the market or economy crashes when one political party is in office. This is because the underlying drivers of market performance – economic cycles, earnings, valuations, etc. – are far more important than who occupies the White House.

That said, policies can certainly affect taxes, trade, industrial policy, regulatory frameworks, and more. However, policy shifts often occur gradually, and their timing and impacts are frequently overestimated. What politicians promise is often different from what is ultimately enacted. Thus, investors should focus on long-term economic and market trends rather than daily poll results.

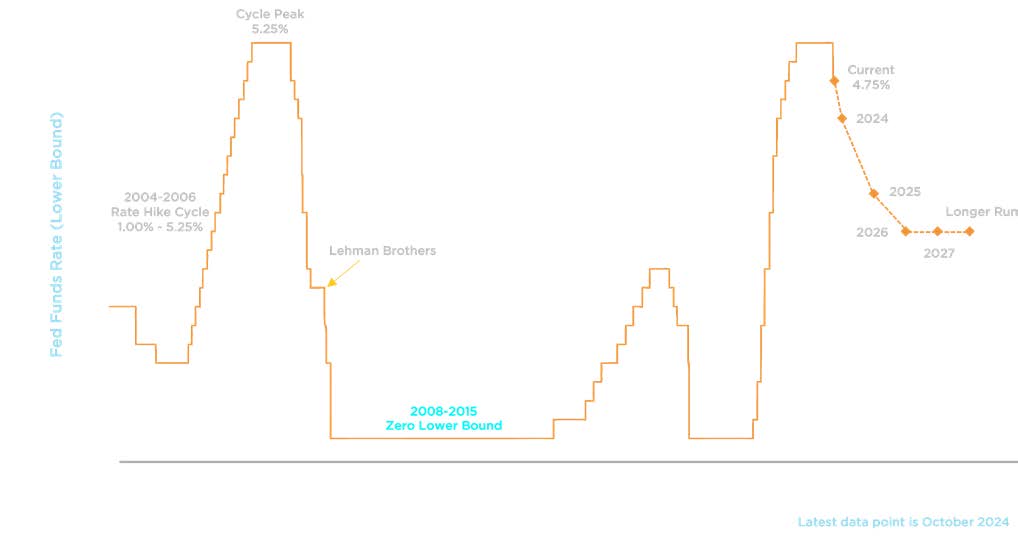

3. The Fed is expected to cut rates further

3. The Fed is expected to cut rates further

Third, inflation continues to moderate, with the most recent data showing the PCE price index, the Fed’s preferred inflation measure, increasing just 2.2% from a year earlier, approaching the Fed’s target rate of 2%. The labor market showed continued signs of slowing through August, though it remained low by historical standards.

These economic conditions, particularly the labor market data through August, prompted the Fed to implement its first 50-basis-point rate cut in September. The market has been anticipating cuts of various sizes all year and rallied in the days following the announcement.

4. The fixed income landscape is shifting

4. The fixed income landscape is shifting

Fed rate cuts have resulted in lower interest rates across maturities, as well as a “disinversion” of the yield curve. This is sometimes referred to as a “bull steepener” since it can be positive for bonds. In many ways, this is a reversal of the bear market in bonds experienced in 2022 when rates were on the way up.

For the economy, lower rates improve borrowing costs for corporations and individuals, potentially boosting economic expansion and investment prospects. This can be positive for economic growth which then translates into better earnings and corporate fundamentals. Thus, despite the challenges bonds have faced in the past few years, it’s important to maintain balance across asset classes.

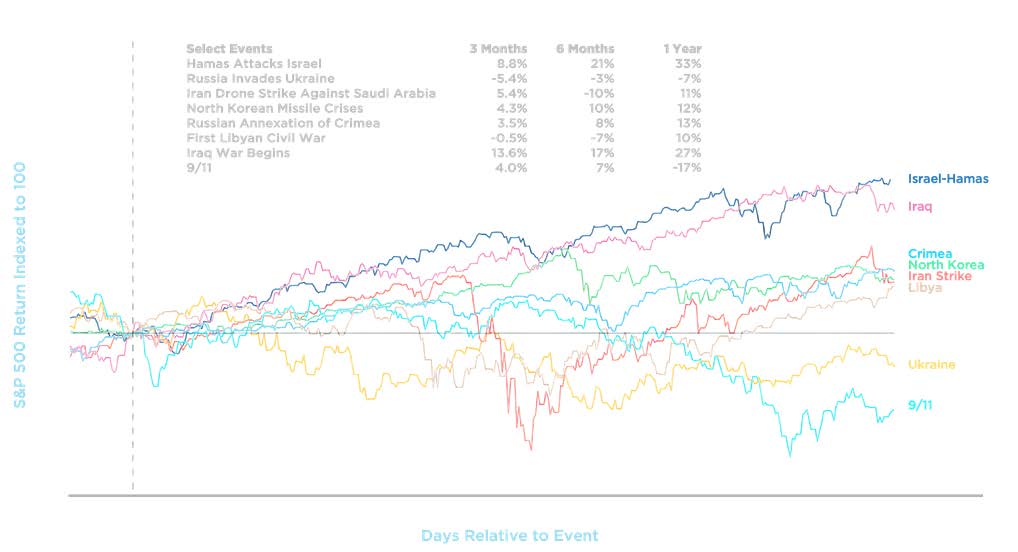

5. Geopolitical conflicts are worrisome but do not directly impact markets

5. Geopolitical conflicts are worrisome but do not directly impact markets

Finally, tensions have risen in the Middle East as the conflict between Israel and Hezbollah has intensified. This adds to global geopolitical tensions including the ongoing war between Russia and Ukraine. While these events have major real-world impacts, their effects on the economy and stock market are less clear cut, and any impact on investors’ portfolios is typically fleeting. One channel through which regional conflicts can impact the broader economy is oil prices. The escalation in the Middle East has caused a slight rise in oil prices, but the increase is modest compared to previous crises, and the U.S.’s position as the world’s

largest oil and gas producer may provide some insulation from global events.

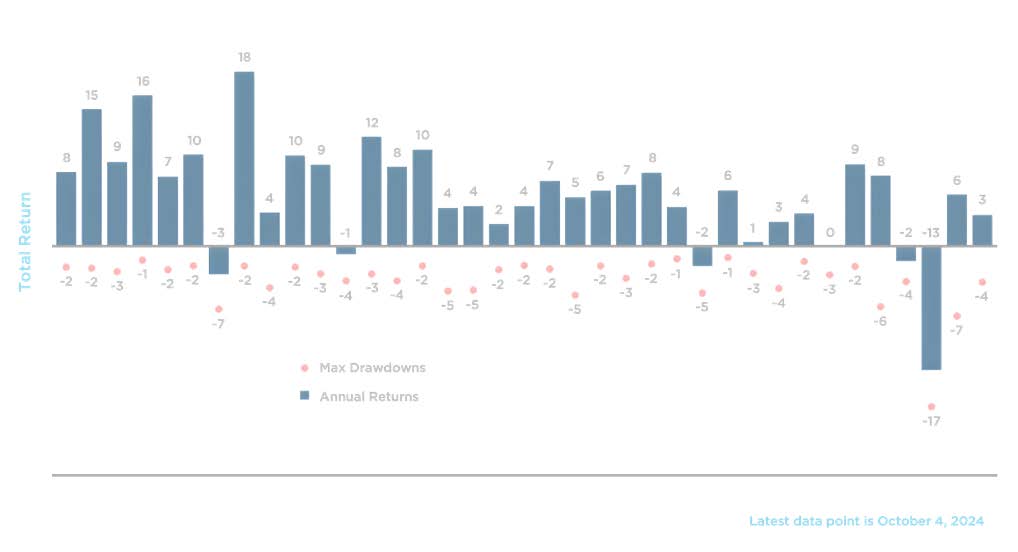

Despite geopolitical uncertainties, the stock market has experienced only two 5% or worse pullbacks this year, emphasizing the importance of staying invested and focusing on broader market trends rather than reacting to headlines.

The chart highlights the top-performing sectors in Q3 2024, with Utilities, Real Estate, and Industrials leading the way. The Federal Reserve’s easing of monetary policy significantly benefited sectors like Utilities and Real Estate. In particular, the utility sector saw strong gains driven by the growing adoption of AI and the surging demand for power from data centers.

Meanwhile, the Industrial sector has been bolstered by economic resilience, with further gains anticipated due to upcoming fiscal spending.

Meanwhile, the Industrial sector has been bolstered by economic resilience, with further gains anticipated due to upcoming fiscal spending.

At Clarien, we strategically positioned ourselves overweight in Utilities and Industrials, allowing us to capitalize on most of these gains. Additionally, we are increasing our exposure to the Real Estate sector, as we believe it still has room for growth, especially given the Fed’s current interest rate outlook.

The bottom line? With the Fed cutting rates, the election on the horizon, and markets near all-time highs, it is more important than ever to stay focused on long-term financial goals rather than short-term events.

Continue to watch our updates for more investment and financial strategy advice. If you have further questions, email us at PrivateWealth@clarienbank.com.