The author Fyodor Dostoevsky once wrote that “man only likes to count his troubles; he doesn’t calculate his happiness.” The idea that the glass is always half empty perfectly captures how many investors feel about the economy and financial markets, especially over the past few years. During recessions and bear markets, investors worry that the situation will never improve. When the economy and markets do recover, investors worry that it won’t last. In both cases, investors often find it difficult to stick to their long-term financial plans, regardless of the historical record. In today’s strong market environment, how can investors stay focused and invested?

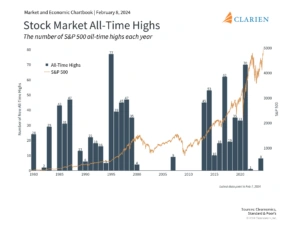

The market has achieved several new all-time highs this year

First, it’s important to understand that it is not unusual for the market to reach new highs during a bull market. By definition, since markets trend upward over long periods, bull markets spend much of their time at new record highs. The accompanying chart shows how frequently these occur during market cycles. From 2013, when the S&P 500 recovered from the 2008 financial crisis, to 2021, the average year experienced 38 days closing at new all-time highs, or roughly 15% of trading days. Years such as 2017 and 2021 experienced many more. Thus, new all-time highs are not, on their own, reasons to be worried about the market or a signal that the market is about to reverse.

First, it’s important to understand that it is not unusual for the market to reach new highs during a bull market. By definition, since markets trend upward over long periods, bull markets spend much of their time at new record highs. The accompanying chart shows how frequently these occur during market cycles. From 2013, when the S&P 500 recovered from the 2008 financial crisis, to 2021, the average year experienced 38 days closing at new all-time highs, or roughly 15% of trading days. Years such as 2017 and 2021 experienced many more. Thus, new all-time highs are not, on their own, reasons to be worried about the market or a signal that the market is about to reverse.

The stock market has achieved several new all-time highs this year following last year’s bull market recovery. The S&P 500 and Dow Jones Industrial Average are now 2.0% and 3.6% above their previous peaks from early 2022, respectively. While this is positive for investors, it’s natural to also wonder whether markets have run up too far, too fast. After all, it was less than a year ago when many investors and economists were predicting a recession and worrying about the rapid pace of Fed rate hikes. In this context, there are three important facts to keep in mind.

Second, what matters is not the level of the market, but the business cycle and underlying trends. While there is still much uncertainty today due to inflation and the timing and size of Fed rate cuts, market sentiment has improved due to steady economic growth. This has driven rallies in technology-related sectors, including across the so-called Magnificent Seven stocks, as well as in areas such as Industrials, Financials, and Health Care.

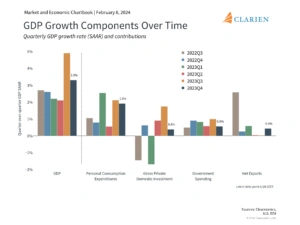

In particular, the latest GDP report for the fourth quarter of 2023 showed that growth was stronger than expected at 3.3% quarter-over-quarter, exceeding economist expectations of only 2.0%. This means that real GDP (adjusted for inflation) grew by 2.5% across all of 2023, one of the fastest growth rates over the past decade. Consumer spending, business investment, government spending, and trade all contributed to these results. In the long run, these factors drive markets more than day-to-day headlines and short-term swings.

The economy grew at a healthy pace in 2023

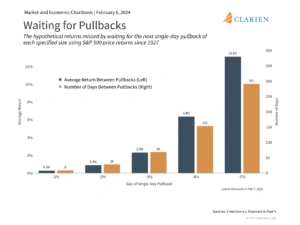

Finally, while it’s natural for investors to feel that they should wait for a market pullback before investing new cash or returning to the market, history shows that this can often backfire. The chart below measures the “opportunity cost” of being out of the market and waiting for a better price, compared to simply staying invested.

Finally, while it’s natural for investors to feel that they should wait for a market pullback before investing new cash or returning to the market, history shows that this can often backfire. The chart below measures the “opportunity cost” of being out of the market and waiting for a better price, compared to simply staying invested.

Waiting for a 3% pullback, for instance, has required being out of the market for 69 days on average across history. Over that period, the market rose much more than 3%, resulting in a missed opportunity of a 2.3% gain. In other words, it would have been better to simply have stayed in the market the whole time. Waiting for a 5% pullback requires 291 days and results in a missed opportunity of 13.1%. Similarly, waiting for 10% market corrections or 20% bear market crashes can take years. In all cases, the peace of mind that comes from sticking to a plan, rather than trying to time the market perfectly, is an added benefit.

It’s often better to stay invested than wait for a pullback

Unfortunately, doing so requires battling our own tendency to see the glass as half empty when markets are rallying. Of course, none of this is to say that the market only moves up in a straight line during bull markets. Investors should always be prepared for market swings and unexpected events, as the past few years have demonstrated. However, it does suggest that it’s often better to avoid making rash decisions based on news headlines and the level of markets, and focus instead on sticking to a well-constructed portfolio, ideally with the guidance of a trusted advisor.

Unfortunately, doing so requires battling our own tendency to see the glass as half empty when markets are rallying. Of course, none of this is to say that the market only moves up in a straight line during bull markets. Investors should always be prepared for market swings and unexpected events, as the past few years have demonstrated. However, it does suggest that it’s often better to avoid making rash decisions based on news headlines and the level of markets, and focus instead on sticking to a well-constructed portfolio, ideally with the guidance of a trusted advisor.

The bottom line? The market has achieved several new all-time highs this year due to steady economic growth. Investors should continue to stay focused and invested and not make decisions based on the level of major market indices alone.